The 9 Benefits of Investing in Real Estate: 2. Appreciation via inflation

When I first began investing in real estate, I did not understand the real impact of inflation (or dollar devaluation) on real assets, how it is designed into our system by the Federal Reserve, and how that impacts your investments. So, let’s take a look at the visual price of property appreciation and the real cost of interest in a system that has built-in dollar devaluation or inflation.

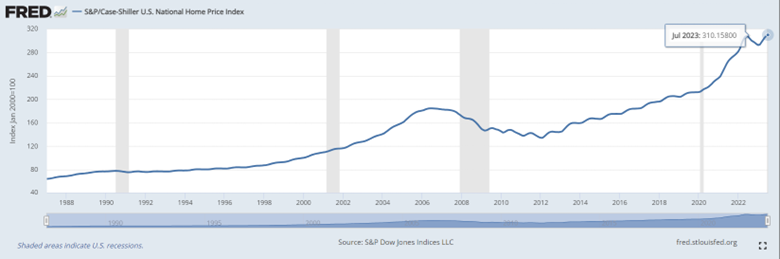

Based on the cost of gas, goods, labor, and a host of other things, prices generally float upward due to supply and demand or currency devaluation which causes asset appreciation. Leaving supply and demand aside, we will consider dollar devaluation (i.e.. Inflation) and how it affects a real asset like a $100,000 house. For example, the Case-Shiller index indicates that real property has appreciated approximately 4% over the last 30 years, so let’s work with that.

(S&P Dow Jones Indices LLC, S&P/Case-Shiller U.S. National Home Price Index [CSUSHPINSA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CSUSHPINSA, October 13, 2023)

Most investors generally put 20% down in a real estate purchase and then mistakenly think that they only make 4% (the average appreciation rate) on their 20% down. However, if you own a $100,000 rental house and the market “inflates” at 4%, as it has on average over the last 40 years, then the property value of the entire asset would grow by 4%, not just the down payment amount. So, let me ask, would you rather have 4% on a $20,000 investment or 4% on a $100,000 investment? The former would become $800 on a $20,000 investment versus $4,000 on a $100,000 asset. By using the leverage of a small down payment and benefiting from inflation on the entire asset – ON PAPER, you make a 20% return on your $20,000 investment ($4,000(asset appreciation)/$20,000 (down payment) = 20%).

Why is appreciation and leverage important? Because if you compare purchasing a $100,000 single-family home with a $20,000 down payment, versus putting $20,000 in the stock market over the same 30-year period you will see the true power of leverage and inflation combined (not to mention the years of cash flow from rents, depreciation from taxes and principle paydown).

For example, if we give Wall Street twice the advantage with 8% a year growth of a $20,000 investment and an average property appreciation of 4% with rent growth of only 1% per year over 30 years, then the stock value will grow to become $186,345 in non-tax advantaged wealth (that you could not touch for those 30 years lest you short circuit its growth), whereas a $100,000 home would be valued at $311,865 after 30 years with only a $20,000 initial investment

Giving the real asset a paltry 4% appreciation rate, it would have increased $211,865 in value to become worth $311,865. But wait, there is more! A tenant would have paid off all the debt ($80,000 in this example), as well as you would have enjoyed tax-advantaged income from the cash flow during those 30 years using a simple 27.5-year straight-line depreciation schedule, unlike your untouchable money in the Wall Street casino. Thus, your real increase would be the $211,865 in appreciation plus the $80,000 loan payoff by another, plus any positive cash on cash received while rented. Even if we ignore the cash flow in our calculations, then the average annual return would be 18% better returns than stock market returns and 32% better than the stock market when the cash flow is considered (even with only 1% rent increases). This is considering just one simple single-family investment. Could you do more????

If we add some zeros and consider buying a $1M asset with $200,000 down vs putting $200,000 in the casino called the stock market and leave all other inputs the same, then the end result after 30 years would be a net worth of $1.8M in stock value vs. a net worth of almost $3.2M in real estate. Real wealth is built from real assets. I have included a simple illustration to compare the differences.

Tell your 401k plan that you want to put $20K into it, receive approximately $2,400 yearly in tax-free cash on cash distributions for the life of the investment, build $4,000 yearly in equity from appreciation, and another approximate $1,000 ($80,000 30-year loan at 6% used for calculation) from someone else (by way of paying down your mortgage) and see how that stacks up. If you can wrap your head around this paragraph and the simple Excel illustrations provided, then you will see the wealth-building power of real assets versus paper. Meaning you put $20,000 into an example single-family home and got back $6,800 in the first year of ownership in the form of cash on cash ($2,400), principal reduction ($1,000), and asset appreciation ($4,000). That is a 34% return ($6,800/$20,000). Compare that to 8% on $20,000, in the untouchable during your healthy lifetime, the stock market of $1,600 if you are lucky.

Asset appreciation is a powerful wealth builder and real estate is realistically the only real hedge against inflation. Considering the data from sources like the Case-Shiller index or even your own experience confirms that those properties generally go up over the long term, along with the rents, via inflation (or dollar devaluation) and will hedge you against rising prices by keeping your passive income moving upwards during retirement years with inflation and your lifestyle intact through increases in rental income.

When I am trying to make my money work smarter and harder for me, then I have to realize that if I leave my $20k in a bank, CD, Bond (if not tax-advantaged), or whatever earning say 4%, it amounts to $800 in non-taxed advantaged income. If I had $200,000 in the bank at 4% then I would earn $8,000 in non-tax-advantaged income. However, with real estate, if the value of the entire property goes up by 4%, then I am making 4% on the entire $100K or $1M asset, not just my $20k or $200k used to acquire the asset. As stated before, that would be $4,000 in equity for a $20k investment or $40,000 for a $1M property. Which would you rather have added to your net worth $800 or $4,000? $8,000 or $40,000? Ask yourself, “Why do the rich get richer?” Generally speaking, it’s because the wealthy own hard assets that appreciate!

For example, my very first rental purchase was a 2 bedroom, 1.5 bath townhome that we paid around $36K for. That was right about 1999 right after I got my real estate license. I don’t remember what the cash flow was or even if I calculated everything correctly and anticipated all the expenses I incurred. But I do remember shaking in my boots over the 20% down of like $7,000 and the mortgage debt of approximately $28k. My biggest fear was that a tenant wouldn’t pay, and I would have to cover two mortgages. I laugh now and realize that you can barely buy a decent vehicle for that amount. I ultimately overcame my fear by considering what that $7k in the bank would do for me. Maybe it would make $70 in interest (or $50 after taxes) in a good year with a stiff wind. Ha. On the other hand, since we did choose to buy that rental property and as time moved on, we eventually sold that first rental property for around $175k about 5 or 6 years later, thanks to inflation or dollar devaluation. Good thing we put that $7k to work when we did. Maybe you think prices are high now? Ask yourself what you think the house next door will cost 20 years from now. Ask any “old-timer” what things used to cost back in the day or what they paid for their home or investment properties. I hear it often and will repeat it, “Don’t wait to buy real estate, buy real estate and wait,” and “It’s not about timing the market, but rather about time in the market.”